LPs’ willingness to back healthcare specialty funds.

Apparently Atlas will soon find out. As its partners part ways, each side aims to raise its own fund: roughly $265 million—the same as the current general fund—for the biotech side, and $125 million for the tech side, according to Fortune. The biotech side will keep the Atlas name, and Booth, who explained the split in public, said the biotech and tech sides were facing “rapidly diverging business models.”

In a follow-up exchange with me, Booth said that the breakup wasn’t about performance; that both sides of the house have had similar returns from recent funds (a claim that’s difficult to verify independently), and that industry returns as outlined by the Cambridge data had no effect on the decision, either. When asked for other reasons, he said “augmenting our footprints in our respective sectors,” “more nimble sector governance,” and “clarity around message and mission” were big factors in the split.

Lightstone’s Carusi echoed some of Booth’s rationale for specialization, and added his own reasons as well.

“I was a big believer in balanced funds,” says Carusi, using another name for diversified funds. But he’s seen the two sides struggle to understand each other’s business models, underlying technology, and culture. The biotech side prefers the experience of “gray haired folks” to run their startups, he says, while the tech side is “often looking for bright young entrepreneurs with unique insights on how to disrupt markets.”

The Lightstone team will continue to manage their old ATV and Morgenthaler investments, but anything new is coming from the $172 million fund Lightstone raised in 2012.

I don’t want to give the impression that diversified funds are an idea of the past. There are still plenty of huge funds investing prolifically and creatively in both information technology and biotechnology. And there are plenty of reasons for firms that house tech and healthcare teams under one roof to keep them that way. First and most obvious: “If it ain’t broke.” New Enterprise Associates, Canaan Partners, Polaris Partners, and Venrock are a few well-known names, and all have raised funds of $450 million or more since 2012. (NEA tops them all with its $2.6 billion fund in 2012.)

I had Canaan’s Wende Hutton (healthcare) and Dan Ciporin (tech) on the phone last week to talk about their new $675 million fund, which, like previous funds, should be roughly two-thirds tech, one-third healthcare. I asked what’s kept the 28-year-old firm together through recent years; Ciporin noted first that “we happen to like each other and get along well.” (Atlas’s Booth wrote something similar about his colleagues in 2012 when explaining why Atlas, in raising its ninth fund, was sticking together: “First and foremost, we like each other.”)

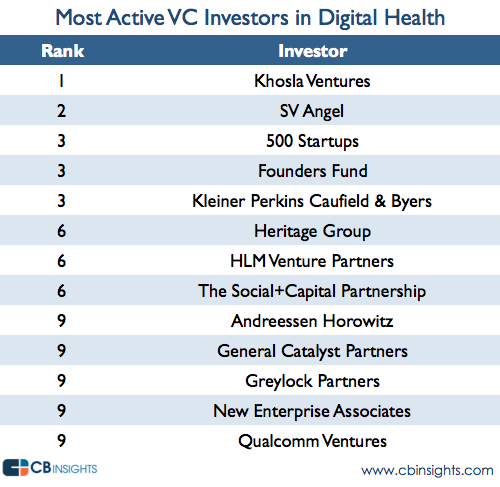

Hutton and Ciporin, who specializes in financial and e-commerce investments, then noted that another reason for staying under one roof is digital health, which in some cases requires expertise from both sides of the house. (Canaan hasn’t participated much yet but looks to do more.) Digital health—or health IT, as some prefer—might indeed be the next hunting ground for big, diversified firms. Investment in the field is taking off, but so far tech-only investors are out in front, with only a couple diversified firms among the ten most active.

{kind=link}

Venrock is not on that list, but when I asked people which diversified firms are building a strong digital health practice, Venrock kept coming up. The firm’s partner Bryan Roberts is one of the few life-science veterans to move aggressively into digital health—he’s the chairman of Castlight Health (NYSE: [[ticker:CSLT]]) and on the board of a few others—but he surprised me with a contrarian view.

Speaking from an airport security line, he told me he thought the tech side of venture would continue to dominate the deal flow in digital health, and diversified firms (like his own) would hold no particular advantage in sourcing deals and building companies. The tech folks, he said, can build software and service companies and look for outside advisors for the requisite healthcare expertise.

Meanwhile, others on the life science side worry about falling behind. Aisling Capital founder Dennis Purcell, whose life-science-only firm mainly invests in later-stage companies and assets, says he sees tech investors like Andreessen Horowitz and Khosla Ventures “making big bets” and wonders if they are “the future of life science.”

“I have to think about what the VC world will look like in five years,” says Purcell. “If it’s toward digital health, who’s ahead of the curve?”

And no matter what strategy is dictated by culture, or fund structures, or degree of difficulty in any particular sector, there’s always that gnawing fear in venture of not being ahead of the curve. Or, as Venrock’s Roberts puts it: “If you go super-specialized, how do you see the next wave of what’s interesting?”